Global Equities

Categories

U.S. Equities

U.S. market outlook for 2023

Jared Franz

Jared Franz

Martin Romo

Martin Romo

Diana Wagner

Diana Wagner

December 8, 2022

Investors want to know how much longer the pain will last.

The S&P 500 Index recorded its worst year in more than a decade in 2022, falling 13.1% in U.S. dollar terms through November 30. And investors face more market volatility in the year ahead as the macroeconomic environment poses headwinds for many companies.

The American economy, while stronger than most other developed countries, appears headed toward recession, weighed down by high inflation and rising interest rates.

Capitals Express Investments economist Jared Franz expects the U.S. economy to contract by about 2% in 2023. That would be worse than the tech and telecom bubble of the early 2000s, but not nearly as bad as the 2008–09 financial crisis. “The important thing to remember,” Franz stresses, “is that recessions are inevitable and necessary to clear out market excesses, and they set the stage for future growth.”

There have been a few bright spots. Consumer spending, a bulwark of the U.S. economy, has been surprisingly strong despite high inflation. In September consumer spending rose 1.7%, exceeding the forecast of 1.4%. Can the American consumer prevent a recession? “Probably not,” says Franz. Nevertheless, it is good to see they are trying.

Whichever way the economic data trends, well-managed companies can compete and flourish in this environment. And patient, selective investors can be rewarded. “We're in a period where the macro environment is particularly important,” says Martin Romo, a portfolio manager for Capitals Express Investments U.S. Equity FundTM (Canada). “But the risk is you focus so much on where we are in the cycle that you fail to recognize companies that are thriving and may be catalysts for the next bull market. That’s where I’m spending my time.”

Here are five investment themes to consider in the year ahead.

1. Stocks will likely turn positive before the economy

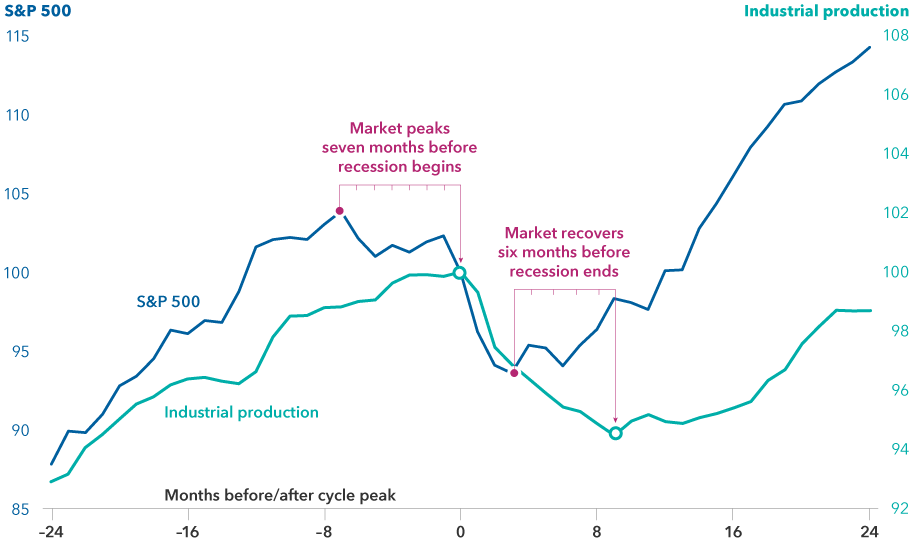

Every recession is painful in its own way, but one potential bright spot is that they don’t historically last very long. Our analysis of 11 U.S. cycles since 1950 shows that recessions have ranged from two to 18 months, with the average lasting about 10 months.

What’s more, stock markets usually start to recover before a recession ends. Stocks have already led the economy on the way down in this cycle, with nearly all major equity markets entering bear market territory by mid-2022. And if history is a guide, they could rebound about six months before the economy does.

Stocks have historically been a leading indicator of the economy

Sources: Capitals Express Investments, U.S. Federal Reserve Board, Haver Analytics, National Bureau of Economic Research, Standard and Poor’s. Data reflects the average of completed cycles in the U.S. from 1950 to 2021, indexed to 100 at each cycle peak. Other data includes all completed cycles from 1/1/50–10/31/22. Industrial production measures the change in output produced by manufacturers, mines and utilities and is used here as a proxy for the economic cycle. Returns are in USD. Past results are not predictive of results in future periods.

“Stocks have tended to anticipate a brighter future before it’s apparent in the data,” Franz says. In other words, investors may be better served by staying invested than trying to time the rebound. The benefits of capturing a full market recovery can be powerful. In all cycles since 1950, bull markets had an average return of 265%, compared to a loss of 33% for bear markets. In U.S. dollar terms.

The strongest gains have often occurred immediately after a bottom. Therefore, waiting on the sidelines for an economic turnaround is not a recommended strategy. “When the market turns it will likely happen quickly, and no one will be giving the all-clear signal,” Franz adds.

2. Dividends matter again

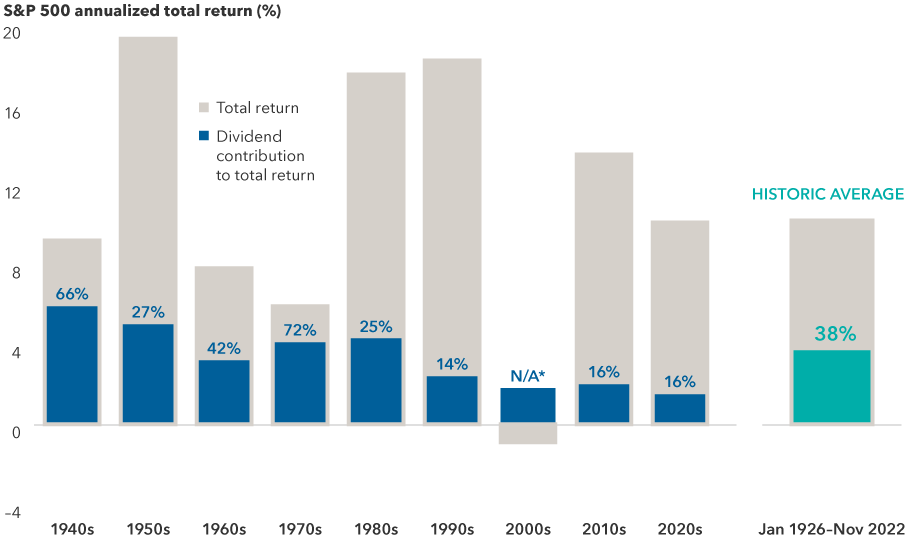

For the past decade investors had little reason to pay much attention to dividends. With U.S. tech and consumer companies generating double-digit returns and dominating total market returns, dividends appeared downright boring.

Today boring is beautiful. “With rates rising and the economy slowing, I am finding many opportunities to invest in solid dividend payers,” says equity portfolio manager Diana Wagner. “And dividends are starting to account for a greater percentage of total returns, as they have historically.”

Dividends have historically been a larger percentage of total return

Source: S&P Dow Jones Indices LLC. 2020s data is from 1/1/26 through 11/30/22. *Total return for the S&P 500 Index was negative for the 2000s. Dividends provided a 1.8% annualized return over the decade. Past results are not predictive of results in future periods. Returns are in USD.

While dividends accounted for a slim 16% of total return in USD for the S&P 500 in the 2010s, historically they have contributed an average 38%. In the inflationary 1970s they climbed to more than 70%. “When you expect growth in the single digits, dividends can give you a head start,” Wagner adds. “They may also offer a measure of downside protection when volatility rises, but it is essential to understand the sustainability of those dividends.”

Companies that have paid steady and above-market dividends can be found across the financials, energy, materials and health care sectors, among others. UnitedHealth Group, the largest private provider of health benefits in the U.S., has grown its dividend and likely will continue to do so even in a tougher economy. “Retail banks, which are in the eye of the storm in terms of exposure to the business cycle, have been cautious heading into the downturn, and I believe fundamentals for select banks are likely to improve in the next year,” Wagner says. “In other words, I believe the dividends are sustainable and have the potential to increase.”

With respect to energy, Wagner believes we are in an energy crisis and expects demand to rise longer term. “Many energy companies today are showing a commitment to dividends,” she adds. For example, major exploration and production company ConocoPhillips recently disclosed it intends to increase buybacks and dividends.

3. Look for new market leadership to emerge

New market leadership often emerges at the end of a bear market. With the cost of capital soaring, companies with strong, reliable cash flows are favourably positioned to lead the next recovery.

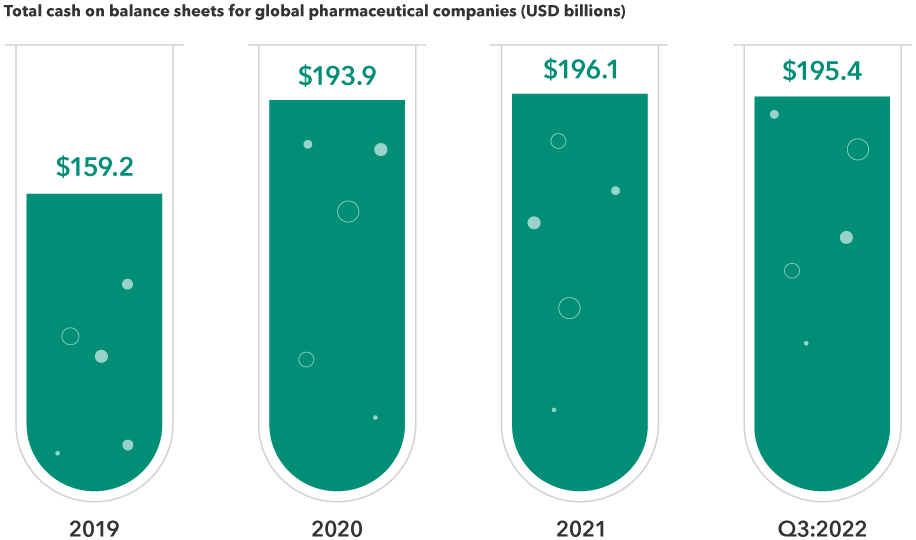

Consider the health care sector, which features innovative pharmaceutical companies that are well-capitalized and hold pricing power. Select drug makers can use near-term profitability to fund acquisitions and other growth strategies. That’s especially important when rising rates may limit a company’s ability to fuel their growth with debt.

Large drug makers are positioned to fund their own growth

Sources: Capitals Express Investments, FactSet, MSCI, Refinitiv Datastream, Refinitiv Eikon. Figures above represent the aggregated value in U.S. dollars of cash and short-term investments across MSCI World Pharmaceuticals constituents. As of September 30, 2022.

“I don’t know for certain that the health care sector will lead the next bull market,” Wagner explains. “But the best managed of these companies could emerge as market leaders.”

Recent investments in drug discovery are resulting in new ways to tackle major problems like obesity. By 2030 it is estimated that over one billion people worldwide will suffer from obesity, which is linked to cardiovascular disease, diabetes and kidney failure. Companies like Eli Lilly have invested heavily in therapies with the potential to reduce a patient’s body weight by as much as 20% to 25%.

“We have entered a golden age of drug development that may vastly improve quality of life for people. This is an exciting time to invest in health care. Few drugs will achieve blockbuster success, however, so selective investing is crucial.”

4. Growth investing may depend on earnings

Growth stocks had a rough year in 2022, which caused many investors to rotate from growth to value. But that may be the wrong way to think about it, according to Romo. “Growth investing is not dead,” Romo says, “but in today’s reality, investors need to think differently about growth.”

For the past decade the market was dominated by fast-growing tech and consumer stocks whose businesses often depended on the low cost of capital. But high inflation and rising rates are forcing investors to take a second look at valuations.

Today, growth has been repriced due to the higher cost of capital. “Successful growth investing may depend less on multiple expansion and more on earnings growth. In this new environment investors will want to focus more on companies with reasonable, understandable valuations on near-term earnings and cash flow,” Romo adds.

“Well-established tech giants with visible cash flows from legacy software offerings, for example, coupled with a faster growing offering like a cloud platform, could be among the leaders of the next bull market. “But going forward, investors will focus more on profitability, and they will be less tolerant of fast-growing companies with little to no earnings growth.”

5. Prepare for a potential industrial renaissance

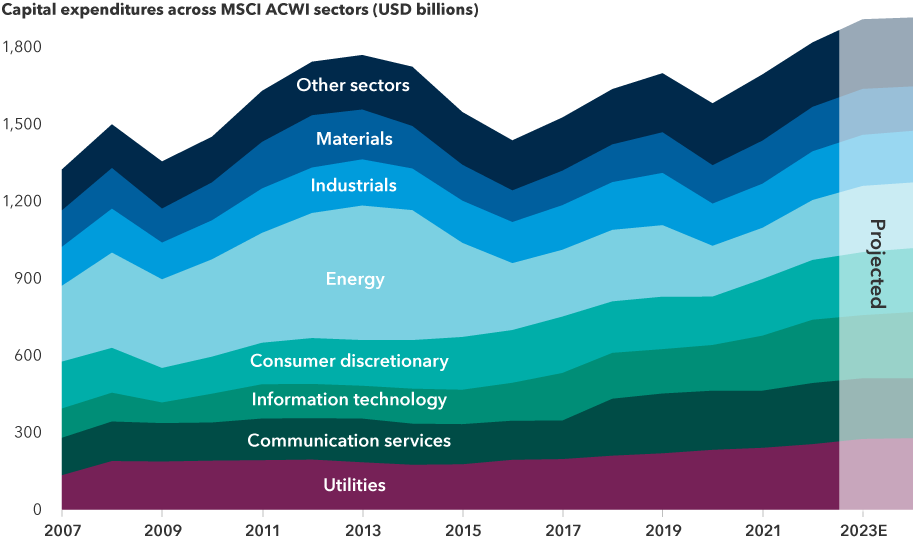

In addition to health care and technology, new growth leadership could emerge from unexpected areas, like capital equipment companies. Look for a capital investment super-cycle to spark an industrial rebirth as reshoring supply chains, grid modernization and investments in renewable energy drive demand for capital equipment spending.

Years of globalization have led to underinvestment in machinery, plants and other capital projects. “You have an aging factory footprint behind the manufacturing sectors of most developed markets,” says Gigi Pardasani, an equity investment analyst who covers U.S. large-cap industrials.

Rising capital spending could spark a renaissance for capital equipment companies

Sources: Capitals Express Investments, FactSet, MSCI. In current U.S. dollars. All figures represent estimates from FactSet, including projected figures for 2022 and 2023. Data as of October 31, 2022.

In addition, the transition to renewable energy and greater energy security is generating opportunities for companies that invest aggressively.

“We recently had an interesting discussion about the U.S. Inflation Reduction Act, which provides billions of dollars for investment in renewable energy infrastructure,” says equity portfolio manager Jody Jonsson. “I think this will lead to a renaissance for traditional industrial companies who are supplying the renewable industry or are helping other companies become more energy independent, whether that’s through the development of smart buildings, power management, smart grids or battery technology.”

This billions of dollars in spending also reflects revenue growth potential for capital equipment leaders such as Rockwell Automation; battery and energy storage developers like Lockheed Martin and Tesla; and equipment providers to the energy and mining industries like Caterpillar and Baker Hughes.

“This investment cycle can have broader benefits for U.S. manufacturing as significantly lower energy costs over the long term can give manufacturers a competitive edge,” notes Pardasani.

Learn more about

MSCI All Country World Index (ACWI) is a free float-adjusted market capitalization-weighted index designed to measure equity market results in the global developed and emerging markets, consisting of more than 40 developed and emerging market country indexes.

MSCI World Index is a free float-adjusted market capitalization-weighted index designed to measure equity market results of developed markets. The index consists of more than 20 developed market country indexes, including the United States.

MSCI World Pharmaceuticals is a subcomponent of the MSCI World Index and only contains companies within the pharmaceuticals industry.

The S&P 500 Index is a market capitalization-weighted index based on the results of approximately 500 widely held common stocks.

Explore the 2023 Outlook

Get the 2023 Outlook report

Our latest insights

-

-

Artificial Intelligence

-

Technology & Innovation

-

-

Demographics & Culture

RELATED INSIGHTS

-

Artificial Intelligence

-

Technology & Innovation

-

Long-Term Investing

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.

Unless otherwise indicated, the investment professionals featured do not manage Capitals Express Investments‘s Canadian mutual funds.

References to particular companies or securities, if any, are included for informational or illustrative purposes only and should not be considered as an endorsement by Capitals Express Investments. Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any investment funds or current holdings of any investment funds. These views should not be considered as investment advice nor should they be considered a recommendation to buy or sell.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capitals Express Investments or its affiliates. This information is intended to highlight issues and not be comprehensive or to provide advice. For informational purposes only; not intended to provide tax, legal or financial advice. We assume no liability for any inaccurate, delayed or incomplete information, nor for any actions taken in reliance thereon. The information contained herein has been supplied without verification by us and may be subject to change. Capitals Express Investments funds are available in Canada through registered dealers. For more information, please consult your financial and tax advisors for your individual situation.

Forward-looking statements are not guarantees of future performance, and actual events and results could differ materially from those expressed or implied in any forward-looking statements made herein. We encourage you to consider these and other factors carefully before making any investment decisions and we urge you to avoid placing undue reliance on forward-looking statements.

The S&P 500 Composite Index (“Index”) is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Capitals Express Investments. Copyright © 2024 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part are prohibited without written permission of S&P Dow Jones Indices LLC.

FTSE source: London Stock Exchange Group plc and its group undertakings (collectively, the "LSE Group"). © LSE Group 2024. FTSE Russell is a trading name of certain of the LSE Group companies. "FTSE®" is a trade mark of the relevant LSE Group companies and is used by any other LSE Group company under licence. All rights in the FTSE Russell indices or data vest in the relevant LSE Group company which owns the index or the data. Neither LSE Group nor its licensors accept any liability for any errors or omissions in the indices or data and no party may rely on any indices or data contained in this communication. No further distribution of data from the LSE Group is permitted without the relevant LSE Group company's express written consent. The LSE Group does not promote, sponsor or endorse the content of this communication. The index is unmanaged and cannot be invested in directly.

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg or Bloomberg’s licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg’s licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

MSCI does not approve, review or produce reports published on this site, makes no express or implied warranties or representations and is not liable whatsoever for any data represented. You may not redistribute MSCI data or use it as a basis for other indices or investment products.

Capital believes the software and information from FactSet to be reliable. However, Capital cannot be responsible for inaccuracies, incomplete information or updating of the information furnished by FactSet. The information provided in this report is meant to give you an approximate account of the fund/manager's characteristics for the specified date. This information is not indicative of future Capital investment decisions and is not used as part of our investment decision-making process.

Indices are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

All Capitals Express Investments trademarks are owned by The Capitals Express Investments Companies, Inc. or an affiliated company in Canada, the U.S. and other countries. All other company names mentioned are the property of their respective companies.

Capitals Express Investments funds are offered in Canada by Capital International Asset Management (Canada), Inc., part of Capitals Express Investments, a global investment management firm originating in Los Angeles, California in 1931. Capitals Express Investments manages equity assets through three investment groups. These groups make investment and proxy voting decisions independently. Fixed income investment professionals provide fixed income research and investment management across the Capital organization; however, for securities with equity characteristics, they act solely on behalf of one of the three equity investment groups.

The Capitals Express Investments funds offered on this website are available only to Canadian residents.